Continuous Cover – It doesn't work

-

Étude de marché 19 août 2022 19 août 2022

-

Asie-Pacifique

-

Assurance et réassurance

Notwithstanding that continuous cover is one of the most important, but controversial, areas of Australian insurance law, there has been very little judicial authority on the issue. That is why the recent decision in CIMIC Group Ltd v AIG Group Ltd & Ors[1] is important in determining the meaning and effect of continuous cover clauses, particularly in the context of multi‑layer insurance with different layers and different insurers on different policy years.

The decision also determines how continuous cover operates in conjunction with an insured's duty of disclosure and whether the equitable right of contribution[2] is available between insurers on different years. Overall, we consider that Justice Peden made the right determinations, but not necessarily for the right reasons.

Continuous cover operates when an insured knew of relevant circumstances[3] in one policy period and yet only notifies that circumstance or resultant claim in a subsequent policy year. Even if the insured had the same insurer across those years, it could still be uninsured for the claim, with no cover under the year the circumstance was first known (because no notification was made to that policy)[4] and be excluded from cover under the policy in which notification is eventually made, by reason of a prior known circumstance exclusion.

The vice which the continuous cover clause seeks to address is the insured's failure to notify a circumstance when first known, which precludes it from cover when subsequently notified. The underwriting intent being that if the insured was continuously insured over that period, it would not fall between policies, and the later policy would provide continuous cover, but subject to the same terms, conditions, exclusions, limitations of the policy under which notification should have first been made. In other words, the insured should get the same cover under the later policy[5] which it would have got if proper notification had occurred.

In CIMIC, the relevant continuous cover clause provided:

"Notwithstanding exclusion 3.2 (Prior Claims and Circumstances), cover is provided under this policy for any claim, or circumstance, which could or should have been notified under any earlier policy, provided always:

(i) the Claim or Circumstance, could and should have been notified after the Continuity Date; and

(ii) the Claim should be dealt with in accordance with all the terms, conditions, exclusions and limitations of the Policy under which the Claim, or Circumstance, could and should have been notified."(our emphasis).

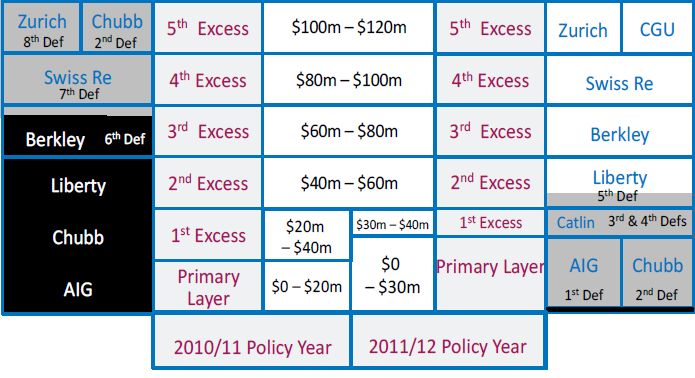

The critical issue in the court’s determination of the Clause was the meaning of the term "limitations", and whether that meant the limit of liability of the first policy, which in this case had been eroded[6], or the uneroded limit[7]. The matter was further complicated because the relevant insurance towers for the two years were not the same. You will see below that in 2010/11 the $20 million primary policy of AIG and first excess of $20 million of Chubb became a combined $30 million primary with AIG/Chubb (50/50) for the 2011/12 year.[8]

Prior to determining the operation of the continuous cover clause, the Court first had to determine whether there was any prior knowledge of relevant circumstances, being the subject matter of a shareholder class action against CIMIC regarding, its failure to disclose known bribery concerns with its Middle Eastern operation, which was also the subject of regulatory investigations and prosecutions.

The relevant facts of the case were:

-

CIMIC[9] had relevant D&O insurance incepting on 30 June of each year.

-

In October 2010[10] a conversation occurred between the co-COO Mr Stewart[11] and the other co-COO Mr Savage in which the latter COO referred to Leighton having paid a significant bribe to obtain an Iraqi contract and was being asked to provide another bribe for the contract’s next phase.

-

Mr Stewart made a detailed file note of that conversation (File Note), noting the seriousness of the issues raised by likening it to the AWB matter[12].

-

The File Note was filed away and resurfaced in late 2011[13] during discovery in a shareholder class action arising from Leighton's significant profit downgrade in April 2011. That shareholder class action was settled in 2014 and, with Defence Costs, eroded circa $75.5 million of the 2010/11 D&O tower.

-

Soon after discovery, the File Note was notified to the AFP and 2011/12 D&O insurers shortly thereafter. There were ASIC and AFP investigations and a resultant second shareholder class action settled in 2019 which caused Leighton to incur loss of approximately $40 million for which it sought indemnity under the 2011/12 Policy. Denial of Indemnity by relevant 2011 insurers.

Denial of Indemnity by relevant 2011 insurers

- AIG, Chubb and Liberty (supported by AXA XL)[14] relevantly denied indemnity on the basis that:

(1) the File Note referencing bribery issues equated to circumstances that may give rise to a claim which ought to have been notified to the 2010/11 policy, and therefore only fell for cover under the 2011/12 year by reason of the continuous cover clause;

(2) the term “limitations” in the continuous cover clause meant the eroded limit of liability of the 2010/11 year, and their limits were entirely eroded;

(3) alternatively, there had been non-disclosure of those circumstances and misrepresentation of the Leighton risk to the 2011/12 insures which entitled them to reduce their liability to nil pursuant to section 28(3) of the Insurance Contracts Act (Cth) (ICA); and

(4) If AIG was liable for any payments under the 2011/12 policy, it was entitled to claim contribution from the 2010/11 insurers – by way of double insurance, on the basis that there were two policies applying to the same loss.

CIMIC's position was relevantly that:

- The File Note was not a circumstance and that cover was available under the 2011/12 policy without continuity of cover.

- If it was a circumstance, the continuous cover clause applied and ‘limitations’ meant the entire limit of liability of the 2010/11 policy was available, without erosion.

- Alternatively, if cover was not available under 2011/12, the File Note was a circumstance which Leighton was entitled to late notify to the 2010/11 policy.

2010 insurers’ position was that:

- The File Note was not a circumstance, such that it could not be late notified to 2010/11 policy – and cover was therefore solely available under the 2011/12 policy without continuity.

- Alternatively, if it was a circumstance, Leighton had elected to seek cover under the 2011/12 policy and was now precluded from seeking cover under the 2010/11 policy.

- The notion of AIG's right to equitable contribution was absurd, particularly as the claim could not be first made under two different years.

The Court held that:

- The File Note referenced relevant circumstances which ought to have been disclosed prior to entry into the 2011/12 policy.

- Cover under the 2011/12 policy was provided by way of the continuous cover clause and 'limitations' meant the uneroded limit of liability of the 2010/11 policy, but cover was also constrained by the eroded limit of 2011/12[15].

- While the court recognised that this could mean that an insured could deliberately not notify a circumstance in order to obtain more cover under a subsequent year, the principles of fraudulent non‑disclosure and breach of an insured's duty of utmost good faith protected insurers from that scenario.

- Availability of cover under the 2011/12 policy was subject to the issue of any non‑disclosure or misrepresentation which occurred prior to the 2011/12 policy incepting, such that the knowledge provisions of the 2011/12 policy[16] did not apply to non‑disclosure or misrepresentation[17]. Relevant knowledge was therefore the common law position of the controlling mind of the Company, ie Board of directors or its agents. Further, a Company could not forget or lose knowledge merely by losing a director, as a Company was deemed always to have that knowledge.

- The 2010/11 insurers led cogent underwriting evidence that had the facts in the File Note been disclosed prior to inception of the 2011/12 policy, they would have each declined to cover any loss arising from those bribery issues – such that the 2011/12 insurers could reduce their liability to nil by reason of prejudice pursuant to section 28(3) of the ICA.

- Leighton could late notify the bribery issues in the File Note to the 2010/11 insurers and Leighton did not make an election between two competing rights in first notifying to 2011/12 insurers and was not therefore estopped from notifying under the 2010/11 policy. Leighton was therefore entitled to a declaration to be entitled to late notify to 2010/11 insurers and such claim was not statute barred.

- If AIG had been liable for loss under the continuous cover clause of 2011/12 it was entitled to rely on section 54 to seek equitable contribution from the 2010/11 insurers, on the basis that there were two policies covering the same loss. The court rejected the notion of a claim not being able to be made under two different years and said the claim was not in respect of a "Claim" but an equitable right of contribution.

- In addition to the non‑disclosure of the content of the File Note, there was also a misrepresentation in the Proposal form that due inquiry had been made of each director about their knowledge of potential circumstances, when clearly that had not occurred. The remedy for that misrepresentation was also prejudice which entitled 2011/12 insurers to reduce their liability to nil.

Our comments on the judgment:

- The Court's interpretation of the continuous cover clause does not correspond with apparent underwriting intention. As above, the intent is to provide the same cover as the Insured would have got under the 2010 year[18] if proper notification had occurred – ie the eroded limit. While the ultimate outcome did not turn on this issue, it will for other cases, particularly where there is no tower of insurance which makes it very difficult to determine the effect of erosion.

An insured should not be put in a better position by its omission and breach of duty of disclosure. The Court recognised that this could cause an insured to deliberately fail to notify/disclose, so as to obtain more cover under a later policy, and said that remedies for fraudulent non‑disclosure and breach of utmost good faith could address that. However, fraudulent non‑disclosure requires discharge of a much higher burden of proof and an insurer ought not be put to such a strict evidentiary test. An insured ought not be able to benefit from its own inadvertent (or deliberate) omission, in obtaining a new limit of cover which would not otherwise have been available to it. Continuous cover is a shield (ie to protect) and should be interpreted as such.

- There has been much differing opinion as to whether continuous cover impliedly waives innocent non-disclosure. While the issue of whether AIG had waived non‑disclosure was before the Court, this was in the context of the non‑avoidance clause – which was held to expressly retain AIG's right to s 28(3) remedies for non‑disclosure in respect of Securities Claims.[19] However, whether continuous cover by itself effectively waives such a right does not appear to have been considered.

- The court held that continuous cover does not by itself waive an insured's duty of disclosure, notwithstanding that the very vice which the clause seeks to remedy is the insured's failure to notify/disclose a known circumstance. It is difficult to see how an insured would ever get the benefit of continuous cover, if that very vice which causes the clause to operate (and which it seeks to remedy – ie a failure to notify/disclose) can be used to deny cover on the basis of non‑disclosure. On that basis, we see continuous cover rarely, if ever, operating[20].

- However, even if continuous cover waived innocent non‑disclosure (and some clauses are worded, such that it could potentially be inferred[21]), that would not necessarily extend to innocent misrepresentation. The court clearly differentiated between the two concepts, such that misrepresentation could still deny the benefit of continuous cover, even if non‑disclosure cannot.

- The Court's acceptance of an insurer's right to double insurance is novel, but justifiable, where the insured has two policies which might provide cover and chooses one. However, it should only operate to allow the later year insurer to seek contribution from the earlier insurer, as the Court held that if the matter had been notified to both years, (or just the first year) the later insurers could rely on the prior known circumstances exclusion to avoid cover.

- The limitation on the application of the deemed knowledge clause for the entity creates a two tier test for insureds and insurers alike. The requisite knowledge to be able to notify a circumstance during the policy period is that set out in the clause (i.e. CEO etc), while for disclosure purposes, it is the common law controlling mind of the company. Different tests can only create confusion and dispute.

Overview

- Continuous cover was considered, but rejected, in the UK insurance reforms however, it remains an important aspect of Australian D&O and Professional Indemnity Policies. Given that importance, it is critical that insurers review their continuous cover wordings to ensure that it accords with their underwriting intent, including whether it should extend to “Claims”[22]; be subject to the lesser of the cover provided under the competing policies (or at least define limitations to include the limit of liability as eroded); expressly retain the right to remedies for misrepresentation and, if necessary, non-disclosure[23]; and also limit an insurers’ liability to only one policy in respect of the same “Claim”.[24] A failure to do so could critically undermine the underwriting intent of later policies, particularly exclusionary wording such as a Fines and Penalties Exclusion which do not occur on earlier policies.

- Cover provided pursuant to late notification is subject to the issue of prejudice. 2010/11 insurers are entitled to argue that they have been prejudiced by reason of the late notification. Whereas the 2011/12 insurers cannot. We see no reason why continuous cover should not also similarly provide for prejudice. There is an absurdity in the same insurer providing different cover for the same Claim – ie late notification with prejudice under year 1 and continuous cover no prejudice under year 2.

- The limitation on the effect of the deemed knowledge clause for the entity has the potential to create confusion about whose knowledge binds an insured entity and in what context. One way to address that confusion is to have the deemed knowledge clause in the Proposal, which is deemed part of the policy documents.

- Further, as always, it is also critical that an insurer is able to lead cogent underwriting evidence of what they would have done if proper disclosure and/or representations and been made, in order to rely on either a non-disclosure or misrepresentation defence.

- This case is not at an end, with further determination of quantum issues to be decided under the policies in which cover was held to be available. We would also be surprised if the important aspects of this judgment were not subject to an appeal.

[1] NSWSC (2022) 999

[2] Double insurance.

[3] Although some continuous cover clauses also refer to claims – which is not required and which we recommend be removed (see below).

[4] If a policy does not contain a contractual deeming clause (which allows the insured to notify a circumstance and then deems any resultant claim to be made at the time of that notification) an insured is unable to late notify a circumstance. Most PI policies omit a deeming clause, while most D&O policies include such a clause which, along with s 54 of the Insurance Contracts Act, allows an insured to late notify a circumstance to the policy when first known. An insured can also rely on s 54 to late notify a claim that first arose during the policy period, even without a contractual deeming clause – which is the reason why there is no need for continuous cover clauses to refer to claims.

[5] Subject to its limit of liability

[6] So as to give the insured the same cover it would have got under the earlier policy.

[7] Which would provide the insured with a new limit of cover.

[8] This meant that if it was the uneroded limit of $40 million how did that translate to the second year.

[9] Then known as Leighton.

[10] During the 2010/11 policy period.

[11] At the time COO of Leighton and CEO from 1 January 2011.

[12] Which involved Iraqi bribery payments and multiple inquiries, claims and prosecutions

[13] During the 2011/12 policy year.

[14] AXA XL also had a rectification argument regarding its stated Continuity Date.

[15] i.e this last point is important as continuous cover cannot turn the $30m 2011/12 primary policy into a $40m policy. Further, it means that if an Insured has two claims afoot over the two years, the availability of cover should not be determined by which settles first.

[16] Which provided that knowledge of Leighton was limited to that of certain officers, such as the CEO, CFO, COO and CLO.

[17] As those contractual provisions only came into existence after the disclosures and representations had been made and relied on.

[18] Subject also to the 2011 Limit of Liability.

[19] Which allows an insurer to reduce its liability to the extent of any prejudice suffered by the non‑disclosure or misrepresentation.

[20] It would only apply if the insurer would have still offered the insurance on the same terms, if correct disclosure/representation had occurred. Continuous cover is the major commercial benefit to an existing insurer which can differentiate it from other insurers.

[21] ie by referencing “in the absence of fraudulent non-disclosure… relevant continuous cover is provided”.

[22] Our view is that it should not as it could turn the policy from a Claims first made and notified policy into a claims notified policy. An Insured has the right to late notify a Claim in any event East End v CE Head (1991) 25 NSWLR400.

[23] But see point 3 above.

[24] To seek to avoid double insurance claims.

Fin