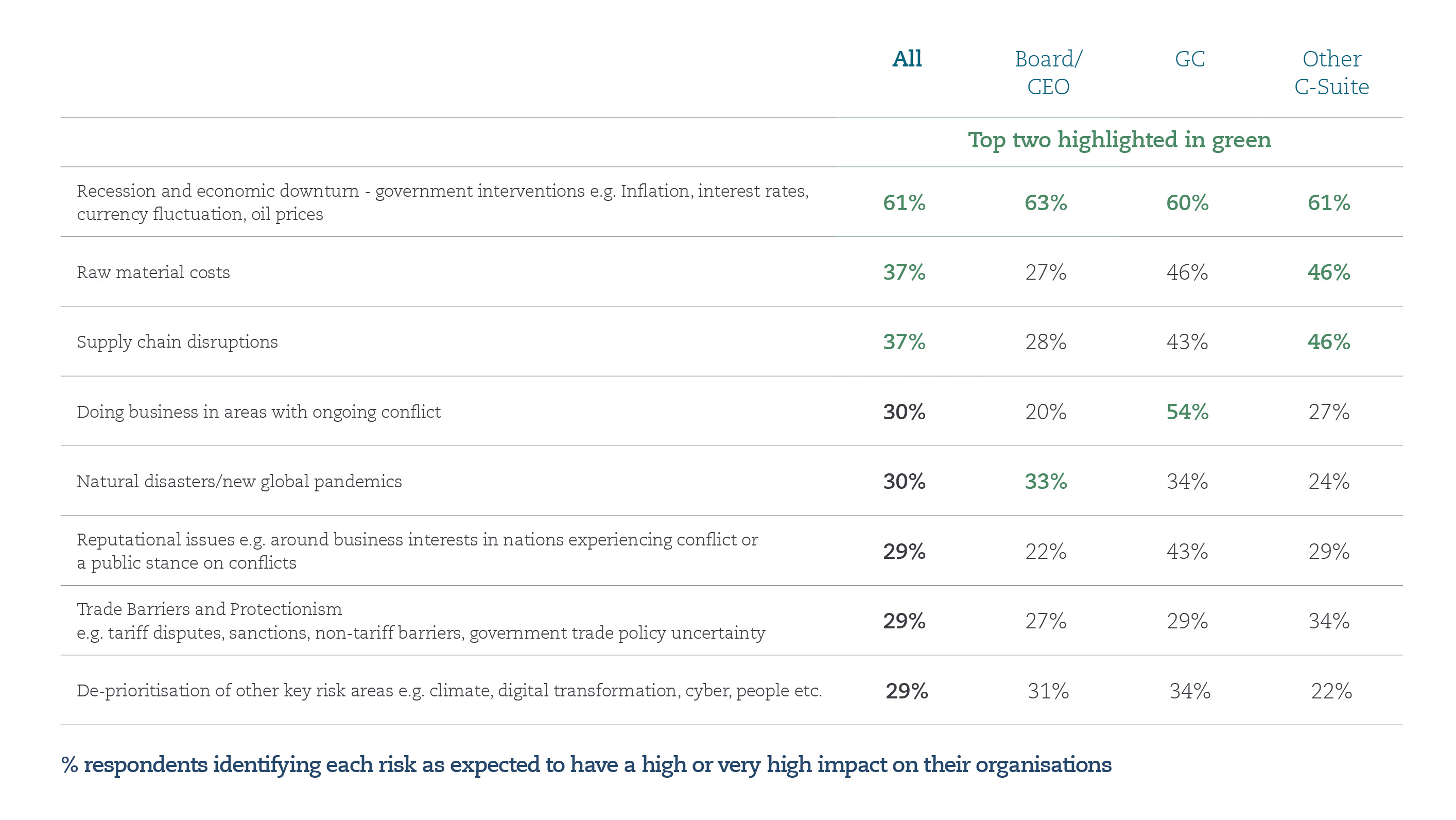

Regulation and compliance continues to be perceived as one of the top three high-impact risks to businesses in the next two to three years, with 58% of senior leaders identifying it as a burden. Somewhat unsurprisingly, this sentiment is most pronounced amongst legal teams, with 74% of general counsels highlighting it as a top risk, a 13% rise from the previous year.

Over two fifths (43%) see the management of regulatory issues as a growing threat, partly driven by a time and budget constrained commercial environment, and some frustration at new regulatory initiatives. Frustration is also expressed at a perceived lack of clarity and certainty in regulatory frameworks, caused by inconsistency and instability amongst some political institutions and governing bodies. 68% said that risk horizon scanning had become a more important part of their role than it was a few years ago.

Businesses across multiple sectors have been grappling with an ever-increasing burden of regulation. This trend has had significant implications for operational efficiency, compliance costs, and strategic planning.

Have you watched our new interactive brochure on our global regulatory & investigations offering?'

Click the link below to view

Regulatory & Investigation interactive brochure

The better the region is regulated, the easier it is for international investors to enter the market, and for regional conglomerates to grow as they can point to the relevant frameworks and rely on the regulations. This might slightly reduce flexibility and freedom to make business decisions or change direction, but regional and multi-national investors have proven to be willing to comply with the rules as they already have the necessary structures in place and see the opportunity for growth.

Roshanak Bassiri Gharb, Partner, Dubai