Hong Kong finalises rules of the risk-based capital regime for insurers

-

Legal Development 08 July 2024 08 July 2024

-

Asia Pacific

-

Regulatory movement

-

Insurance

Enacted by the Legislative Council on 6 July 2023, the Insurance (Amendment) Ordinance 2023 (“IAO”) [1] aims to amend the Insurance Ordinance (Cap. 41) (“IO”) and most notably, implement a risk-based capital (“RBC”) regime for insurers in Hong Kong. Subsequently, on 3 May 2024, the Hong Kong Government published in the Gazette various subsidiary legislations under the IO (“Subsidiary Legislations”) in relation to the detailed rules and technical requirements of the RBC regime. Following such gazettal, the Subsidiary Legislations have come into operation in tandem with the commencement of the IAO and the RBC regime on 1 July 2024.[2]

From the perspective of authorised insurers or prospective insurance business applicants in Hong Kong, the key provisions of the RBC regime are as follows:

1. The Three-Pillar Framework

The RBC regime comprises three pillars which covers different aspects of the RBC regime: The IAO provides the legal basis for Pillar 1 (Quantitative assessment) and Pillar 3 (Disclosure), while Pillar 2 (Corporate governance and risk management) has been implemented with the issuance of the Guideline on Enterprise Risk Management (“GL21”), which took effect on 1 January 2020. For the purposes of this newsletter, we will focus on the requirements under Pillar 1 and Pillar 3.

2. Pillar 1 – Quantitative Assessment

Detailed requirements of Pillar 1 are outlined in the Insurance (Valuation and Capital) Rules (Cap. 41R) (“Cap. 41R”). [3]

The key capital adequacy requirement under the RBC regime is set out in Rule 5(1) of Cap. 41R, which provides that an applicable insurer[4] must ensure its capital base (“Capital Base”) is not less than each of (a) the prescribed capital amount (“PCA”), (b) the minimum capital amount (“MCA”) and (c) HK$20,000,000. Such requirements may be varied or relaxed by the Insurance Authority (“IA”).

Determination of the Capital Base, PCA and MCA

Under Rule 7 of Cap. 41R, the Capital Base composes of Unlimited Tier 1 capital, Limited Tier 1 capital and Tier 2 capital, among which, the Limited Tier 1 capital of an applicable insurer must not exceed 10% of the PCA, and Tier 2 capital must not exceed 50% of the PCA. Only capital resources or instruments meeting the tiering criteria of capital set out in Cap. 41R may form part of the Capital Base.

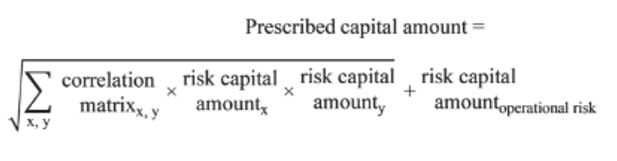

Under Part 5 of Cap. 41R, an applicable insurer must determine its PCA by (a) aggregating the risk capital amounts for its risk exposures to market risk, life insurance risk, general insurance risk, counterparty default and other risk, and (b) adding the risk capital amount for operational risk using the formula set out below:[5]

The following risks are further categorised into sub-risk modules as to which their respective risk capital amount should be aggregated in accordance with the relevant formulas set out in Cap. 41R:

- Market risk: interest rate risk, credit spread risk, equity risk, property risk and currency risk

- Life insurance risk: mortality risk, longevity risk, life catastrophe risk, morbidity risk, expense risk and lapse risk

- General insurance risk: general insurance risk (other than mortgage insurance risk) (reserve and premium risk and general insurance catastrophe risk) and mortgage insurance risk

An applicable insurer should, inter alia, adopt a look-through approach on underlying risk, recognise any insurance risk or financial risk mitigation effect and take into account the effect of loss absorbing capacity of future discretionary benefits and deferred tax in determining the relevant risk capital amounts.

Lastly, pursuant to Rule 5(3) of Cap. 41R, the MCA is determined as 50% of the PCA, or such other amount determined by the IA by way of variation or relaxation.

Actions to be taken in respect of any Contravention of The Capital Adequacy Requirement

Under Rule 6 of Cap. 41R, the applicable insurer must immediately notify the IA in writing on its directors, its controllers or any key person in control functions (a) reaching a view that the insurer is at risk of contravening Rule 5, or (b) knowing or having reason to believe that a contravention by the insurer of Rule 5 has occurred, and provide the IA with particulars of the notified case as required by the IA.

If the level of capital falls under or is at risk of falling under the MCA, the IA may take regulatory intervention actions on solvency grounds, such as requiring the submission of a plan for restoring sound financial position. If the level of capital falls under or is at risk of falling under MCA, the insurer will be deemed insolvent by virtue of Section 42 of the new IO and the IA will need to exercise its strongest powers of intervention, such as requiring the insurer to submit a short-term financial scheme for more immediate remedy.

Valuation of Assets and Liabilities

Part 4 of Cap. 41R prescribes the valuation basis of assets and liabilities as required under the IO. Rules 12 to 32 cover the valuation method of insurance liabilities, whereas Rules 33 to 36 provide the valuation of other items including reinsurance recoverables, deferred tax assets and liabilities, and contingent liabilities.

Transitional Arrangements

Under Part 7 of Cap. 41R, for the purposes of determining its PCA, an applicable insurer may make an application to the IA for approval of a transitional arrangement in reducing its risk capital amount for market risk during a transitional period, i.e. the 36-month period beginning on the date on which Cap. 41R will come into operation.

3. Pillar 3 – Disclosure

Submission of Insurers’ Information to the IA

Under Section 13AA of the new IO, an authorised insurer may be required to report to the IA (including requirements as to how and when) any information relevant to its compliance with the capital requirements. Failure to do so is an offence under the IO and one will be liable on conviction to a fine of HK$200,000, and in the case of a continuing offence, to a further fine of HK$5,000 for each day during which the offence continues.

Detailed requirements of Pillar 3 are outlined in the Insurance (Submission of Statements, Reports and Information) Rules (Cap. 41S) (“Cap. 41S”).[6] Pursuant to Cap. 41S, an authorised insurer should submit, inter alia, to the IA:

- Financial statements as required under the Companies Ordinance (Cap. 622) or required in the place of its incorporation or domiciliation within a specified period of 4 months after the end of the period to which they relate (Rule 3); and

- Annual, quarterly or monthly returns (if any) to be signed or approved by a controller of the insurer, a key person in the financial control function of that issuer, or a director and auditor’s reports in relation to such returns (Rules 4 and 5).

Disclosure of Insurers’ Information to the Public

In addition to the statutory reporting requirements to the IA, an authorised insurer is required to disclose to the public information relating to its state of affairs under Section 21A of the new IO. At present, there is no further elaboration on what public information the insurer is required to disclose to the public.

We will continue to monitor the developments of the new RBC regime. It is expected that further guidance, together with elaborations or practicable considerations of the RBC regime and/or the IAO will be published by the IA in due course.

If you have any questions on any information set out in this newsletter or requires advice on compliance-related issues, please get in touch with Joyce Chan or your usual Clyde & Co contact.

[4] As defined under Rule 3 of Cap. 41R, an “applicable insurer” includes (a) authorised insurers; and (b) any company that makes an application under section 7 of the IO for authorisation. Cap. 41R does not apply to (a) marine insurers and captive insurers, except to the extent provided in the Insurance (Marine Insurers and Captive Insurers) Rules, (b) Lloyd’s, except to the extent provided in the Insurance (Lloyd’s) Rules, or (c) special purpose insurers.

[5] Formula extracted from Rule 37(1)(c) of Cap. 41R.

[6] https://www.gld.gov.hk/egazette/pdf/20242818/es22024281863.pdf.

End