Rapport 2022 sur la croissance du secteur de l’assurance

10 février 2022

Cliquez sur chaque termes pour accéder aux articles correspondants

1. Introduction

Sentiment across the insurance industry is markedly positive, especially in the context of events of recent years. While 2021 saw the pandemic continue to shape the economic and political landscape, rising prices across all product lines, even those perceived as difficult, generated healthy top line growth for many insurance businesses.

Following the release earlier this year of the Insurance Growth Report 2022, which offered an overview and analysis of global insurance M&A across 2021, in this mid-year update our partners across the world examine the trends and factors driving deal activity in the first six months of this year.

In the face of stark economic pressures – inflation, rising energy costs, and looming recession – insurers remain focused on growth opportunities.

Produit

18 août 2022

Écrit par:

Temps de lecture

5 mins

Sujets

Réformes réglementaires

TéléchargerProduit

18 août 2022

Écrit par:

Temps de lecture

5

Sujets

Réformes réglementaires

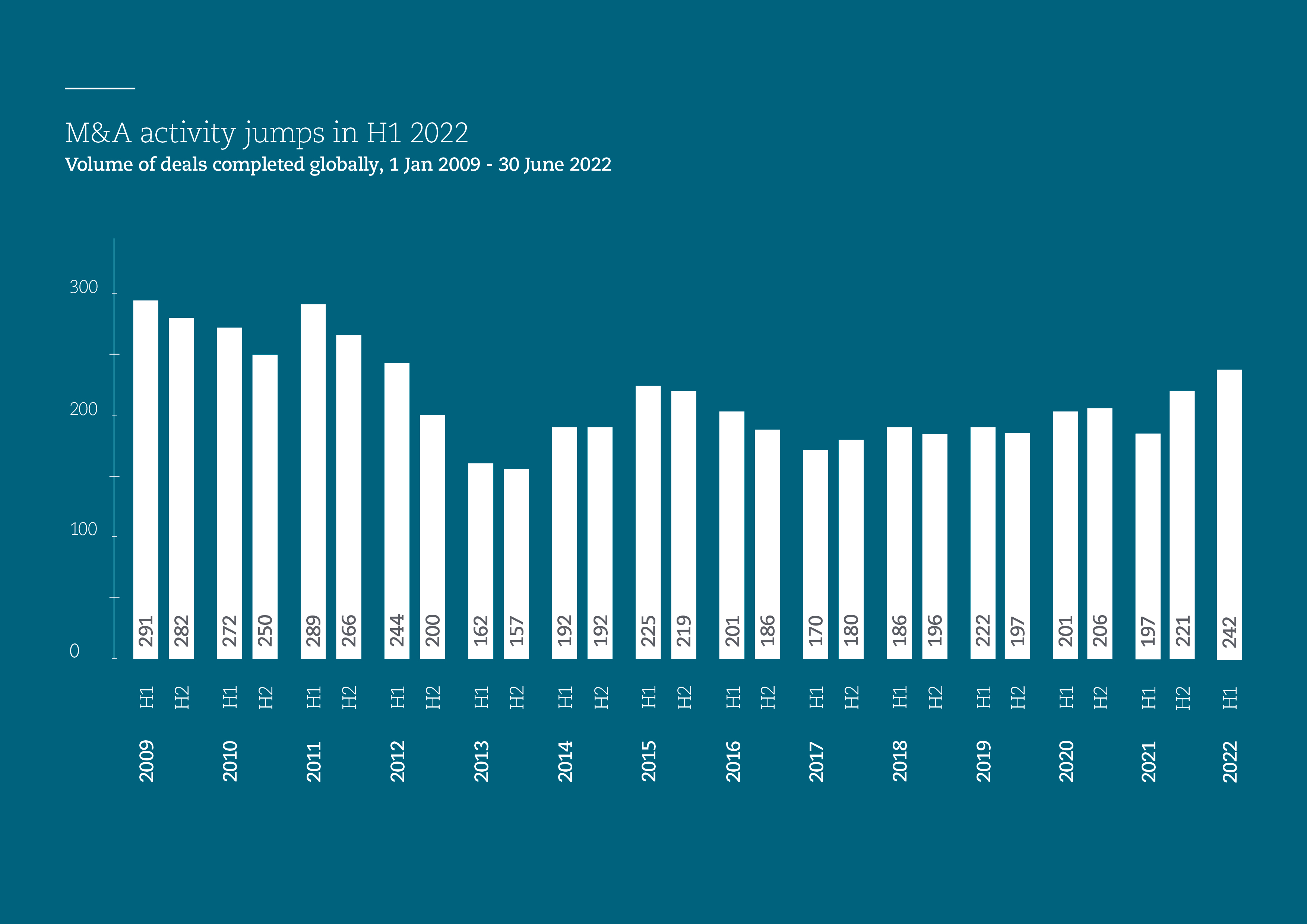

TéléchargerIn the first half of 2022, the volume of mergers and acquisitions (M&A) in the global insurance industry reached its highest rate of growth for ten years.

Key stats at a glance

Five growth factors to watch

Against a testing political and economic backdrop for the insurance industry, carrier sentiment around growth varies across territories and industry sectors.

Private equity interest in the insurance industry remains buoyant, especially with respect to the broker space. Funds are awash with capital and keen to deploy it in a sector they increasingly view as giving attractive and reliable returns.

One area which has seen a significant increase in transactions in the first half of 2022 has been the divestment of non-core assets by carriers, with non-life divestments involving a mixture of spinning off divisions/subsidiaries for sale to third parties, sales of renewals rights, portfolio transfers, and run-off.

Investment into the insurtech sector has soared in recent years, reaching a record level last year, but a decline in the valuation of tech companies which have recently gone public began late last year.

Cyber has seen a boom in both insurance capacity and the creation of specialised brokers and carriers in recent years, but the risk is becoming something of a double-edged sword.

Fin